2025 Annual Market Review

GLOBAL STOCKS END 2025 WITH A STRONG FINISH AS THE FED LOWERS RATES

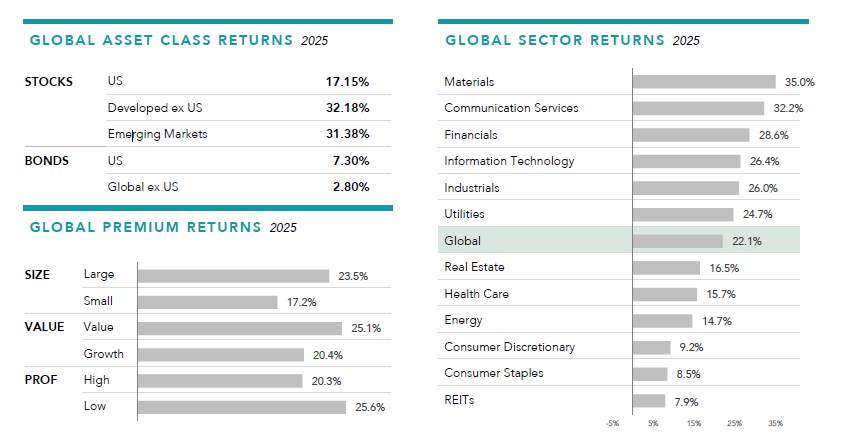

Global equity markets gained during the fourth quarter to finish 2025 with strong returns. The broad Russell 3000 Index was up 2.40% for the quarter to close the year with gains of 17.15%. While 2025 saw a weakening job market, overall growth was resilient, and markets reacted favorably to the Federal Reserve making three additional rate cuts during the later part of the year. Globally, most other central banks decreased policy rates, with the notable exception of Japan.

Technology companies at year’s end were below earlier highs, but the tech-heavy Nasdaq still advanced 20.9% in 2025. Just months after reaching $4 trillion, NVIDIA became the first public company to reach a market capitalization of $5 trillion, though it wouldn’t hold that level. The headline names associated with artificial intelligence have been strong performers in recent years. But diversified equity portfolios don’t need to chase a few big names to have exposure to AI – the technology now touches many types of businesses.

In a departure from recent years, developed international stocks fared better than their U.S. counterparts. The MSCI World ex USA Index gained 31.9%, outpacing the S&P 500 by the widest margin since 1993 and serving as a reminder of the potential benefits of an internationally diversified portfolio. Emerging markets fared even better than developed markets, with the MSCI Emerging Markets Index rising 33.6%. Global equities, as measured by the MSCI All Country World Index, rose 22.3% for the year.

FIXED INCOME

The U.S. Federal Reserve cut the federal-funds rate by a quarter point three times, in September, October, and December, to a range between 3.5% to 3.75%, the lowest level in three years. In its December statement, the Fed cited labor-market worries as it lowered rates while also noting rising inflation and not all members supported the rate decrease. While investors may worry about the impact of Fed rate changes, market interest rates and the federal-funds rate don’t always move as one – the 10-year Treasury yield, for example, hasn’t always gone in the same direction as the fed-funds rate. The Bloomberg U.S. Aggregate Bond Index was up 7.3% in 2025, its best annual return since 2020.

ALTERNATIVES

The Bloomberg Commodity Total Return Index returned +15.77% for the year. Silver and gold were the best performers, returning +152.68% and +57.49% for the year, respectively. Natural gas and sugar were the worst performers, returning -21.88% and -21.11% for the year, respectively. Investors showed increased appetite for gold in 2025 and into early 2026, pushing prices up almost 60% to above $5,000 per ounce for the first time. Some market participants view gold as a hedge during economic downturns or against inflation. But since 1970, gold has often experienced large price swings relative to annual inflation. Over the same period, gold prices showed little relation to fluctuations in the U.S. GDP.

Bitcoin has plummeted from its October 2025 peak of over $126,000 to as low as $60,000 early in the morning of February 6, 2026. After hitting that low, it rebounded to about $70,000 that afternoon. The peak-to-bottom drop represented a more than 50% collapse in just four months. February 5 alone saw Bitcoin drop more than 10%, its steepest single-day decline since the FTX collapse in November 2022.

ECONOMY

Second quarter GDP growth came in at 3.8%, and third quarter growth at 4.3% was the fastest pace in two years, bolstered by resilient consumer and business spending and calmer trade policies. The strength of the economy looks like it continued into the fourth quarter as the Federal Reserve’s current forecast is for growth of 3.0%. Yet job creation has slowed considerably, and unemployment has ticked up. In addition, at a December gathering of CEOs in Midtown Manhattan organized by the Yale School of Management, 66% of leaders surveyed said they planned to either reduce their workforce or maintain the size of their existing teams next year while only a third indicated they planned to hire. One question that author and leading investment advocate Larry Swedroe has been fielding is around concerns with the apparent paradox between robust GDP growth in recent quarters and persistent weakness in labor markets. Swedroe believes the answer is that it isn’t really a paradox at all — it reflects a fundamental structural shift in how our economy generates growth.

Three primary forces are driving the labor market slowdown. First, immigration restrictions and increased deportations have tightened labor supply, removing a traditional U.S. growth advantage. Second, AI implementation is reshaping workforce demand across sectors—eliminating certain positions while driving productivity gains. Third, government employment has contracted. The crucial insight here is that AI adoption simultaneously eliminates jobs and fuels GDP growth through productivity improvements, all while helping contain inflation. Despite labor market softness, Swedroe outlines a few of the powerful tailwinds propelling economic expansion:

The AI Infrastructure Boom – McKinsey projects cumulative AI-related spending will reach $6.7 trillion of the next five years.

Global Investment Surge – International growth has accelerated thanks to aggressive fiscal stimulus and elevated defense spending.

Energy Driven Disinflation – Lower oil prices are exerting downward pressure on inflation.

Consumer Strength – Spending remains strong and should receive an additional boost from expanded tax refunds coming this spring, potentially up to $50 Billion of additional refund above the prior year.

Accommodative Policy – the CBO estimates the OBBB will boost GDP growth by 0.9% in 2026, a central provision allowing business to fully deduct capital expenditures starting January 1, 2026.

While tariffs and trade tensions persist as a headwind, their impact is outweighed by powerful tailwinds from the AI boom and industrial renaissance. The seeming paradox between strong GDP and weak employment reflects a structural shift toward capital-intensive, productivity-driven growth that generates economic expansion without proportional job creation. This dynamic, while challenging for labor markets near-term, could establish the foundation for sustainable, non-inflationary growth over the longer horizon.

LOOKING FORWARD

Looking back often gives us tangible examples of why developing a clear investment plan – and sticking to it – matters, especially as we keep looking to the future. Last year offered another example: Investors who stayed calm and aligned with their plan were in a great position to be rewarded. Here’s how:

If you had gone to sleep on April Fools’ Day and checked your investment portfolio a month later, you might have assumed the market had been relatively calm. However, we all know that was hardly the case. The Trump tariffs were announced on April 2. As of April 8, the broad U.S. stock market had dropped 16 percent. On April 9, a pause in the tariffs was announced and markets bounced back almost 9 percent in single day. Investors who spent the month tracking daily returns, the experience likely felt extremely stressful and disruptive. April 2025 turned out to be one of the most volatile months in recent history, as market participants were processing new information about tariffs and trying to make sense of what the developments might mean for businesses, investors, and the global economy.

It is natural to want to stay informed about what’s going on in the world. And when markets are volatile, it may be hard to resist the urge to do something. But doing nothing – or exercising patience with long-term goals in mind – can be a fine course of action. Thinking about investments over the long term might ease the urge to make hasty asset allocation changes. An investor who stayed the course over the long term – riding out the ups and downs of economic shocks, wars, and other crises – would have seen exponential gains in their investment. Declines can be painful in the moment, but markets have shown resilience throughout history.

SUMMARY

A new year is synonymous with ushering in a renewed optimistic posture, regardless of what the prior year revealed. One way to maintain that optimism, especially in tumultuous and uncertain times, is to have a plan in place when the inevitable, unforeseen events reveal themselves. Again, this is where time we spend with you up front in developing your investment plan pays dividends in the long run.

We appreciate the opportunity to work with each of you. We recognize that each client’s situation – and where they are in their investment journey – is unique and incorporates different factors into their investment and financial plan.

As always, if you have any questions or concerns about current market trends and the impact on your personal situation and plan, please contact us and we would be happy to discuss with you.

Please follow this link to read the complete 2025 Annual Market Review.