The Quarter in Review | 1Q 2026

Markets Navigate A Volatile 2026

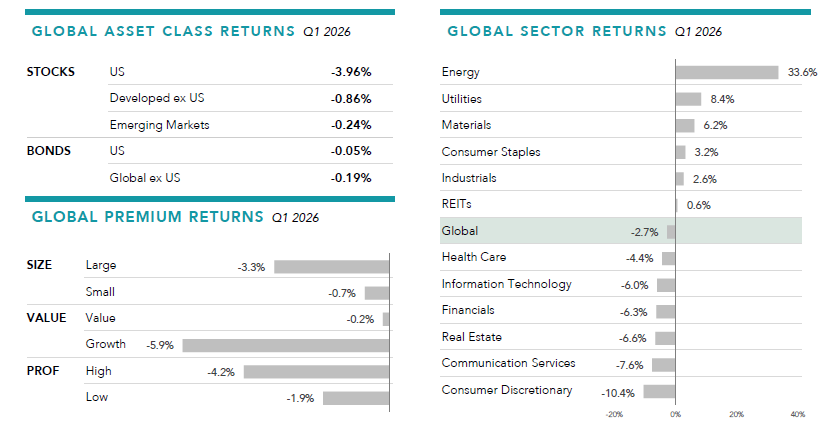

Global equity markets posted a negative and highly volatile first quarter of 2026, weighed down by geopolitical shocks, elevated energy prices, and sharp declines among mega cap growth stocks. Despite a strong rally on the final trading day of March, the period marked the worst start for the S&P 500 Index since 2022, with the index declining 4.3% for the quarter. Broad developed and emerging markets posted negative returns for the quarter but proved more resilient than U.S. stocks.

Performance diverged sharply across sectors. Energy stocks surged more than 30%, driven by supply disruptions and sharply higher oil prices tied to escalating conflict in the Middle East, while technology, consumer discretionary, and financial stocks were particularly hard hit. Mega cap technology names—especially Microsoft, Nvidia, Apple, and Tesla—were the largest individual detractors.

Macroeconomic conditions added further pressure. Inflation remained stubbornly above the Federal Reserve’s 2% target, leading the Fed to hold interest rates steady during the quarter and reducing investor expectations for future rate cuts.

Performance across individual markets was mixed, with wide dispersion in returns across countries. Within developed markets, Japan, Canada, and the UK posted gains for the quarter, while Korea and Taiwan were relative standouts among emerging markets.

FIXED INCOME

Nominal bond returns were slightly negative across major markets, with U.S. bonds returning -0.05% and global ex-US bonds -0.19%. Against a backdrop of geopolitical uncertainty and energy prices leading to elevated inflation risk, U.S. investment grade credit spreads widened modestly but remained historically tight at 0.89% as of March 31. This widening contributed to the Bloomberg U.S. Credit Bond Index underperforming the government index by 0.44%. Municipal bonds also posted modestly negative returns, with the S&P Intermediate Term National AMT-Free Municipal Bond Index declining 0.19%.

In contrast, inflation-protected securities outperformed, as the Bloomberg U.S. TIPS Index returned 0.26%, benefiting from insulation against rising inflation expectations.

ECONOMIC OUTLOOK

There are several forces currently distorting the short-term economic outlook. Taken in the aggregate, it can seem concerning. However, each issue has its unique circumstances and timeframe that is worth looking at individually to understand its impact.

Oil – The Iran war has now entered its third month, with a temporary ceasefire but also a U.S. blockade of Iranian ports, a de facto Iranian blockade of the Strait of Hormuz, and no sign of any resolution of the underlying nuclear issue. Every day the Strait is closed, global oil inventories fall. This has had a somewhat muted impact on oil prices so far, since the world entered 2026 with near-record high stockpiles of oil and oil products. These inventories fell rapidly in both March and April and, if this continues for a few more months, then oil prices could move much higher. However, before this fully plays out, it should become a more urgent issue for the U.S. administration due to the political cost of fast-rising gasoline prices. David Kelly, Chief Global Strategist at J.P. Morgan Asset Management, holds a baseline view in which traffic through the Strait resumes close to normal patterns within the next two months, with global oil prices falling sharply although not to pre-war levels.

On AI Capital Spending – Earnings reports from first-quarter reporting show a further step-up in capital spending plans with the largest five hyper-scalers now expecting to spend roughly $725 billion in 2026 – up from a prior estimate of $675 billion and far above the $416 billion they spent in 2025. To put these numbers in perspective, $725 billion equals just over 60% of all the money spent last year on U.S. home-building and home renovations, while the increase in hyper-scaler capex accounts, on its own, for about 17% of the increase expected in nominal GDP between 2025 and 2026.

On Economic Growth – First-quarter real GDP grew at a 2.0% annualized rate following a 0.5% gain in the fourth quarter. More than 90% of this gain came from increases in business fixed investment in equipment and intellectual property. That should decelerate a little over the rest of this year and in 2027.

Elsewhere, growth is likely to be more subdued with real consumer spending rising at a relatively steady 1.5% rate. Home-building and state and local government spending are likely to grow very slowly, with inventories declining a little, reflecting the impact of the Iran war on energy stockpiles and federal government spending increasing more quickly, due to the need to replace munitions used in the war so far.

Jobs / Unemployment – The current pace of economic growth would normally be associated with monthly job gains of between 100,000 and 150,000. In April, the Bureau of Labor Statistics confirmed the economy added 115,000 nonfarm payroll jobs. However, severe restrictions on labor supply due to lower net immigration could cut job growth to about 60,000 per month, according to Kelly. Even this slower rate of job growth should put some downward pressure on the national unemployment rate, which held steady at 4.3%.

Corporate Profit – As of May 1, with 72% of S&P500 market cap reporting, first-quarter pro forma S&P500 earnings per share were on pace to register an astonishing 24.5% year-over-year gain. However, it should be noted that just three companies have accounted for more than half of this year-over-year increase, largely due to accounting rules that required them to recognize one-time increases in the value of their stakes in AI companies or one-time tax benefits.

Inflation – Kelly believes that some further heating up is likely into the summer but then price increases should recede. In April, the Fed’s preferred measure of inflation, the personal consumption deflator, rose to 3.8% year-over-year and this rise is expected to continue in May to well over 4%.

The Fed and Interest Rates – There has been no recent change in interest rates, as expected, which signals that the Fed is unlikely to reduce rates any time soon, despite constant pressure from the administration and the recent confirmation of Kevin Warsh as Fed Chair. In particular, the decision by three members of the FOMC to vote against the statement because it continued to show an easing bias was a clear signal that the FOMC members won’t vote to ease unless and until they feel the data justify it.

LOOKING AHEAD

Conflict and wars such as the one unfolding in Iran are always disturbing. For investors, there’s additional concern over whether these conflicts will spill over into their investment performance. However, it’s important for investors to be cautious about making asset allocation changes in response to geopolitical conflict.

Markets are forward-looking. Prices move in response to changes in information, and in today’s digital world changes can be daily or even hourly. When unexpected developments arise that investors deem to be unfavorable, markets often drop. But the flip side is markets always set prices for positive expected returns. Once the news gets reflected in market prices, investors can still expect positive returns even amid worrisome circumstances.

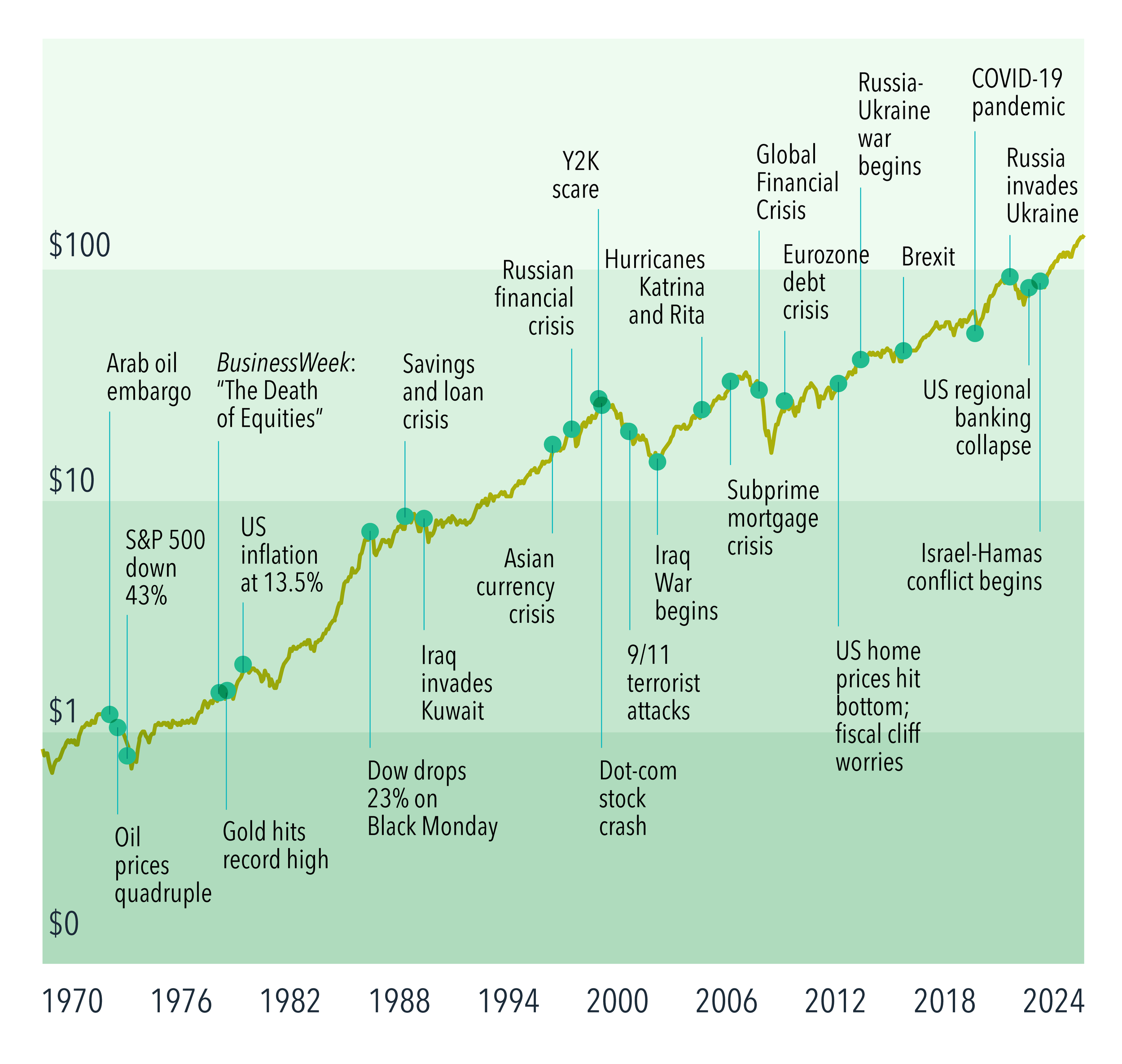

This isn’t hopeful projection; it is borne out of historical stock returns. Global equity markets have continued an upward climb even in the face of economic and political upheavals. We don’t have to look far for illustrative examples. During the past few years, stock markets have had positive returns despite multiple wars being fought around the world.

MARKETS HAVE REWARDED DISCIPLINE

Growth of $1 – MSCI World Index (net dividends), 1970-2025

This is not to trivialize the very real human impact of wars, geopolitical conflict, or other major disasters, whether they are natural disasters or of our own making. But history remains a reliable teacher, suggesting time and again that those who remain diligent and patient in accordance to their investment plan, are better positioned to weather market volatility.

SUMMARY

These are challenging times, and a lot of information is being put in front of us daily to consider. Much of it, as it relates to your investment plan, becomes noise – and a distraction from the disciplined path we charted with you. We can’t predict when unforeseen events will occur, but it’s inevitable that they will.

Again, this is where our time spent with you up front in developing your investment plan pays dividends in the long run. No gimmicks. No shortcuts. Just thoughtful, disciplined investments to meet your long-term goals, while recognizing that every client’s situation and timeframe is unique with its own milestones.

As always, if you have any questions or concerns about current market trends and the impact on your personal situation, please contact us and we would be happy to discuss.

We appreciate the opportunity to work with each of you.

Please follow this link to read the complete QMR Q1 2026.